Aug 3, 2026

Your First Retired Years, On Diversification & Tax-Smart Giving

We suggest that many of the families we meet use some sort of calculator to model their portfolio over the span of their retirement.

Owen Mulhern

Follow Owen Mulhern on LinkedIn

On our docket for today:

Sequence of returns risk: why modeling your retirement on “average” returns is a risky plan

The second reason we diversify: finding winners

How a client used a highly appreciated stock position to fund the charities they cared about, without triggering a capital gains tax bill.

If any of this resonates, please pass it along.

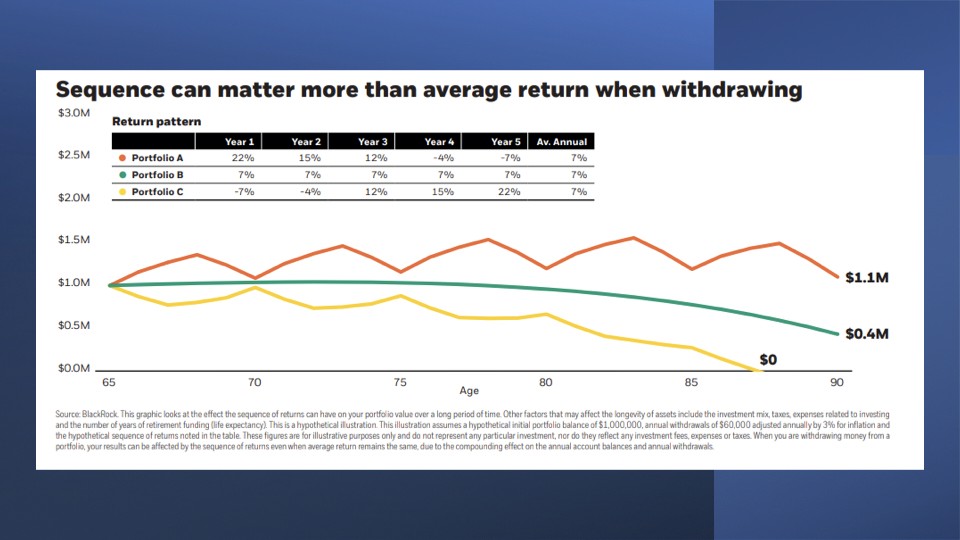

What Is Sequence of Returns Risk?

We would suggest that many of the families we meet initially have used some sort of calculator to model their portfolio over the span of their retirement. You can model different average returns–4%, 7%, 12% sounds great. “If the market returns 6% over 30 years, the math works.”

Here is the problem. The order of those returns matters as much as the average.

Imagine two people retire on the same day with the same amount of money and the same average return over 30 years. One of them gets the bad years early. The other gets them late. The chart below is a model of what that does to their portfolio. (The middle line is the “average”, and all three lines assume $60K withdrawals annually plus 3% inflation.)

The reason is simple. When you are drawing income from a portfolio and the market drops in those first few years, you are selling more shares at lower prices to cover your expenses. Those shares are gone. They cannot participate in the recovery. The portfolio shrinks faster than the math would suggest, and it never fully catches up.

The person who retired in 2008 had a much harder road than the person who retired in 2009. Same strategy. Very different results.

This is why we talk so much about having the right structure in place before retirement begins, not after. Identifying how much income you will need in the near term and setting it aside in something that is not exposed to the market means you are not a forced seller in a down year. The long-term money stays invested. It participates in the recovery. And the unlucky timing scenario, while still uncomfortable, does not permanently damage the plan.

You cannot control when you retire relative to the market. You can control whether you are prepared for the worst case when you get there.

Diversification for the Winners

Look up the Dow Jones from 30 years ago. How many of those companies are still relevant today? How many still exist at all? The version of diversification most people know is about managing risk. Don't put all your eggs in one basket. If one position falls, the rest cushions the blow. That is true, and it matters, but diversification does something else that does not get nearly enough attention. It helps you own the future winners.

The winners change. The companies that led the market a generation ago are not necessarily the ones leading it now. The ones that will dominate in 15 years may be largely unknown today. When a portfolio is concentrated in a handful of names, the investor is not just taking on volatility risk. They are taking on the risk of holding the wrong stocks when the market evolves around them.

A broadly diversified portfolio, rebalanced consistently, means you are always rotating toward the winners as they emerge without having to predict who they will be. We think that is a better use of time and capital than trying to figure it out in advance.

Donating Appreciated Stocks

A client came to us with a position in a high-growth stock that had grown dramatically over the last several years. It had become a significant part of their portfolio, and they did not need it to maintain their standard of living. The obvious move was to diversify. The problem was the tax bill that came with it.

This is something we see regularly with retired clients: a highly appreciated position with an extraordinarily low-cost basis, where the tax consequence of selling is large enough to stop people from doing anything at all. The tax tail wagging the dog.

In this case, we worked through a different option. Rather than selling and triggering the capital gain, we helped the client move the shares into a donor-advised fund (DAF). Within the fund, the position could be diversified without realizing any gains, and the proceeds would fund their charitable giving for years.

The stock that had become a planning problem became the funding vehicle for causes they cared about. Highly appreciated securities are not always a liability. Sometimes, with the right structure, they become one of the most meaningful financial tools a family has.

–––––

The Retirement Paycheck is one part of Your Retirement Gameplan, the planning process we take every client through. If you are heading into retirement and not sure how your income actually works yet, a good place to start is a complimentary conversation with one of our coaches. You can schedule one at financialcoachgroup.com/contact.

Not intended as a recommendation or offer of any specific advice or services. All investments carry risk, and past performance does not guarantee future results. For detailed information about our fees, services, and background, please view our regulatory disclosure materials on the SEC Investment Adviser Public Disclosure Website (https://adviserinfo.sec.gov/firm/summary/170478).

Stay Informed, Retire Confidently

Join our community of savvy retirees and get our latest insights first

Investment Advice offered through FC Advisory LLC, a registered investment adviser doing business as “New Wealth Project” and as “Financial Coach”. This content is provided for informational purposes only. Views and opinions expressed are those of the authors and do not necessarily reflect those of FC Advisory, LLC. Information provided is not and should not be interpreted as investment, tax, legal, or other professional advice or recommendation by FC Advisory, LLC or the members of our firm. Always consult the appropriate professional regarding your specific situation before implementing any options presented or inferred. FC Advisory LLC, All rights reserved.

Read more

Retirement Paychecks, Market Downturns & Variable Income

For most of your working life, your portfolio had one mission: TO GROW. What changes the moment you retire? THE MISSION.

Owen Mulhern

How We Turn 30 Years of Savings Into a Retirement Paycheck

Turning your savings into your spending comes with no obvious roadmap for many families.

Owen Mulhern, CFP®, Partner, Wealth Coach

Caught off guard by a big tax bill?

Most surprise tax bills are usually the result of a few small gaps that went unnoticed throughout the year. Here’s are three steps to reduce the chances of this happening again next year.

Kevin Janiec